Regression Analysis (Testing For Serial Correlation, Durbin Waston Test, Std. Residuals)

Video Not Working? Fix It Now

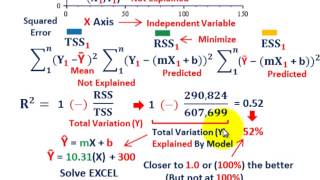

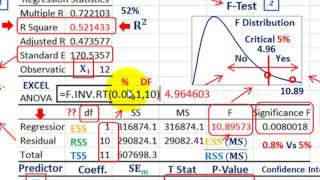

Linear Regression Analysis, testing for serial correlation (Durbin Watson Test) based on Linear regression model for a linear line established by X (Independent Variable) & Y (Dependent Variable), checking for Description, positive vs. negative serial correlation,If Residual (Deviations) are Serial Correlated (+/-), 1-Estimated Regression Coefficients Not Minimized, 2-MSE (Mean Square) may Underestimate Variance Error, 3-Computed Standard Error (Parameter) Underestimated, detailed example by Allen Mursau

Durbin Watson

regression analysis

variance

serial correlation

estimated residuals

mean square

regression coefficients

standard error

regression line

regression

least squares method

goodness of fit

squared errors

independent variable

dependent variable

data analysis

linear line

cost accounting

managerial accounting

excel

cost analysis

forecasting

standard devation

Mursau

linear regression

standardized residuals

Comment