Stata Tutorial: Basics of Instrumental Variables and Two-Stage Least Squares

Video Not Working? Fix It Now

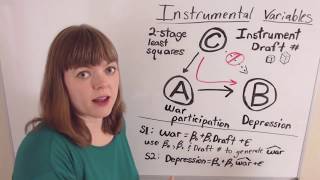

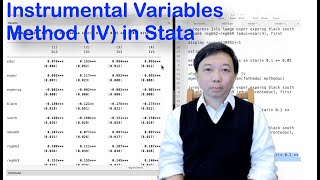

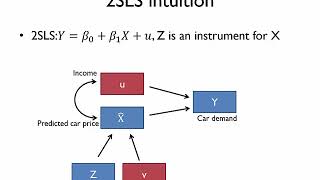

We cover the basic theory and derivations of the Instrumental Variable and Two-Stage Least Squares estimators, then walk through an example of each in Stata.

We use the "ivreg" command, and apply the example to publicly available data accessed through the "bcuse" package.

Link to the excellent Introduction to Econometrics Textbook by AH Studenmund:

https://www.amazon.com/gp/product/9332584915/ref=as_li_tl?ie=UTF8&camp=1789&creative=9325&creativeASIN=9332584915&linkCode=as2&tag=mikejonasecon-20&linkId=6697afcfde8c335b461795eec22e3977

Link to Jeffrey Wooldridge Introductory Econometrics Textbook:

https://www.amazon.com/gp/product/8131524655/ref=as_li_tl?ie=UTF8&camp=1789&creative=9325&creativeASIN=8131524655&linkCode=as2&tag=mikejonasecon-20&linkId=0a5fe7ce6ac777090a194cb5bb48071b

Comment

![1 A.M Study Session 📚 [lofi hip hop]](https://ytimg.googleusercontent.com/vi/lTRiuFIWV54/mqdefault.jpg)