Step-by-Step Portfolio Std Dev and VaR Calculations | Value at Risk

Video Not Working? Fix It Now

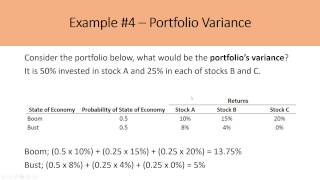

Calculating the Value at Risk (VaR) for two positions requires the calculation of the 'Portfolio Standard Deviation', and in turn, this requires the calculation of the correlation coefficient between positions. This episode explains the full formula and also considers different correlation values as examples to aid understanding.

Understanding the calculation using two positions is a critical step before moving on to look at full portfolio risk management techniques, which can have a dramatic effect on trading.

Brought to you by Darwinex: UK FCA Regulated Broker, Asset Manager & Trader Exchange where Traders can legally attract Investor Capital and charge Performance Fees: https://www.darwinex.com/?utm_source=youtube&utm_medium=video-description-above-fold&utm_content=mt-inst-risk-mgt-12&atp_source=youtube&atp_medium=video-description-above-fold&atp_content=mt-inst-risk-mgt-12

Follow Darwinex on LinkedIn:

https://www.linkedin.com/company/tradeslide-ventures/

#ValueAtRisk, #VaR, #TwoAssets, #TwoPositions, #Correlation, #CorrelationCoefficient, #Pearson, #R, #PortfolioStandardDeviation, #Risk, #Volatility, #PortfolioRiskManagement, #MartynTinsley, #Darwinex

This is Episode 12 in the Darwinex 'Institutional-Grade Risk Management Techniques' Playlist: https://youtube.com/playlist?list=PLv-cA-4O3y979Ltr9wQ2lRJu1INve3RCM

Video Contents:

00:00 Calculating VaR for 2 Assets

00:24 Why Darwinex?

01:13 Portfolio Std Dev and Correlation

01:33 Benefits of Portfolio Risk Management

03:24 Value at Risk Calculations

05:48 Portfolio Standard Deviation Calculation

08:23 Impact of Correlation on Std Dev

10:57 Summary and Next Episodes

Content Disclaimer: Past performance is not a reliable indicator of future results. The contents of this video (and all other videos by the presenter) are for educational purposes only and are not to be construed as financial and/or investment advice.

Risk disclosure: https://www.darwinex.com/legal/risk-disclaimer

Comment